An Interview with Carl Gordon, Managing Partner, OrbiMed Advisors

- Georges HAZAN

- Nov 23, 2025

- 5 min read

Updated: Nov 25, 2025

OrbiMed is a global healthcare investment firm that finances companies across all stages of the life sciences sector, from early-stage biotechs to large pharmaceutical enterprises.

How would you describe the current investment climate for the biotech sector? Do you believe the difficult period the industry has faced in recent years is finally coming to an end?

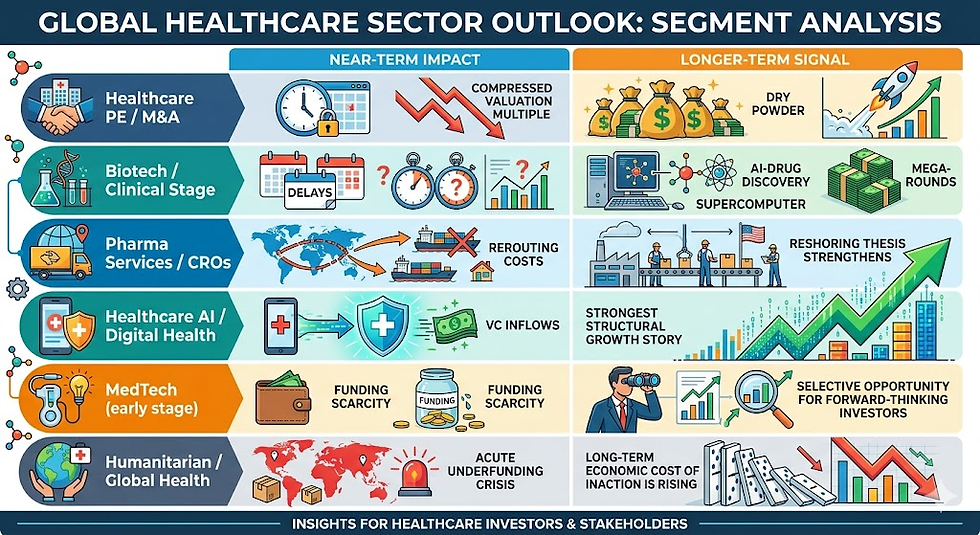

I think it’s an exciting time for the sector. It’s never easy to be a biotech investor, but over the last several months, the climate has improved significantly. The XBI index is a good indicator—it’s now just over 100, up from the high 60s at its lowest point. That’s roughly a 50% increase from the trough. So yes, I do believe we’ve turned a corner in biotech for a number of reasons.

What are those reasons? Earlier this year there were concerns about the low number of IPOs and M&As in the sector. What has changed?

On the macro side, there have been two major positive developments. First, interest rates have come down—both long-term and short-term—which is hugely important for early-stage biotech, a sector defined by long-duration assets. The Fed has also indicated potential further cuts, improving companies’ ability to raise capital.

The second positive factor relates to policy. Some of the Trump administration’s measures have turned out to be more positive—or at least neutral—for the industry. Concerns around tariffs, for example, have largely not materialized. Companies like Pfizer and AstraZeneca have reached agreements with the administration to avoid tariffs, and that could set a precedent for others. So, both lower interest rates and constructive policies have been supportive for the industry.

Don’t you think Trump’s more ad hoc, direct approach to negotiating with companies creates uncertainty for investors?

I think as long as the administration achieves its objectives while enabling companies to succeed, it’s positive. So far, that balance seems to be holding, and I think we’re in a good place overall with continued innovation and growth of US biotechnology.

And what about the ongoing discussion around lowering drug prices? How has that affected investor interest in biotech?

Governments everywhere are interested in reducing drug prices, and that’s something our industry must live with. At OrbiMed, we focus on investing in highly innovative companies developing transformative products—those tend to be less exposed to short-term policy shifts. More specifically, the Trump administration is encouraging other wealthy countries to pay more for drugs to reduce price discrepancies with the U.S. We’ve already seen companies like Eli Lilly, BMS, and Pfizer responding by working to raise prices in Europe.

OrbiMed recently raised almost $2 billion for its Healthcare Royalty and Credit Fund V, which provides non-dilutive capital. How does that fit into your broader investment mix, and do you expect this type of financing to grow in importance?

Our vision is for OrbiMed to serve as a one-stop shop for healthcare financing at every stage—from seed funding for two scientists in a lab to structured credit and royalty monetization for mature companies. Beyond capital, we aim to be hands-on partners, helping portfolio companies with strategy and operations.

The royalty and credit approach is particularly attractive to companies that have raised substantial equity and want to avoid further dilution, or those that believe they’re undervalued by the market and prefer non-equity capital. So yes, this type of structure is a key part of our platform and a growing pillar of life sciences finance.

How do you identify companies that are performing well but are undervalued by the market? What criteria guide your investment decisions?

We conduct deep due diligence on both the science and the management team. We look for companies developing something truly innovative—programs that can change the course of medicine. We also leverage our extensive network to understand a company’s reputation and potential.

Alongside scientific rigor, we place a strong emphasis on management quality—leaders with integrity and proven track records. When both the science and leadership align with our standards, we’re confident in moving forward.

How involved are you operationally with your portfolio companies?

It depends on the situation. In our venture capital business, we typically take board seats to help shape strategy. In some cases, we assume direct operational roles—sometimes even founding companies ourselves and deploying OrbiMed team members with operational expertise to run them. Most often we guide companies from the board level, but occasionally we take a very “hands-on” role.

Could you share an example that illustrates OrbiMed’s investment philosophy or hands-on approach?

A good example is SpringWorks Therapeutics, which was acquired by Merck KGaA earlier this year. The company originated from assets spun out of Pfizer, and we played a major role in setting it up. Several of our team members were directly involved operationally in its early stages. We also helped place a senior OrbiMed team member as acting head of R&D, brought in additional investors during subsequent financing rounds, and supported the company through to its IPO. It’s a strong example of how we engage to help companies succeed. Today our portfolio includes more than 100 such companies.

Given current geopolitical tensions, especially with China, how do you assess and manage related risks when investing?

China’s biotech industry has grown rapidly over the last decade, but the U.S. remains the global leader. Chinese firms often focus more on high-quality follow-on products, whereas U.S. companies excel in innovation and first-in-class drugs. For U.S. players, being a “fast follower” has become more challenging, so focusing on breakthrough innovation is key.

We remain confident in the U.S. biotech sector and assess the global landscape carefully to identify companies best positioned for success within that broader context.

From your perspective, which U.S. life-science subsectors are currently underappreciated?

There are two ways to look at it: by therapeutic area— we’re excited about neuroscience, obesity, and immunology—or by modality, where we find RNA, small molecules, and protein drugs compelling.

Lately, orphan-drug areas serving small populations have been less in favor. Encouragingly, under FDA Commissioner Martin Makary, the agency has shown willingness to ease approval paths for such drugs.

Gene therapy is another area where enthusiasm has cooled due to some setbacks.

But at OrbiMed, we cast a wide net across all modalities and therapeutic areas, always searching for the “diamond in the rough.” We don’t write off any category entirely.

Do you believe biotech’s best days are still ahead?

Absolutely—emphatically yes. We’re strong believers in this industry and proud to contribute to it. Our mission at OrbiMed is to help turn extraordinary science into medicines that improve lives.

The science today is astonishing, with breakthroughs in RNA-related drugs, gene editing, and other new modalities. Our job is to help translate these discoveries into real-world therapies, and we’re confident the most exciting days for biotech are still to come.

Comments