BROTHERS & Partners 2025 Investment Trends

- Georges HAZAN

- Dec 22, 2025

- 3 min read

'Looking Back & Forward''

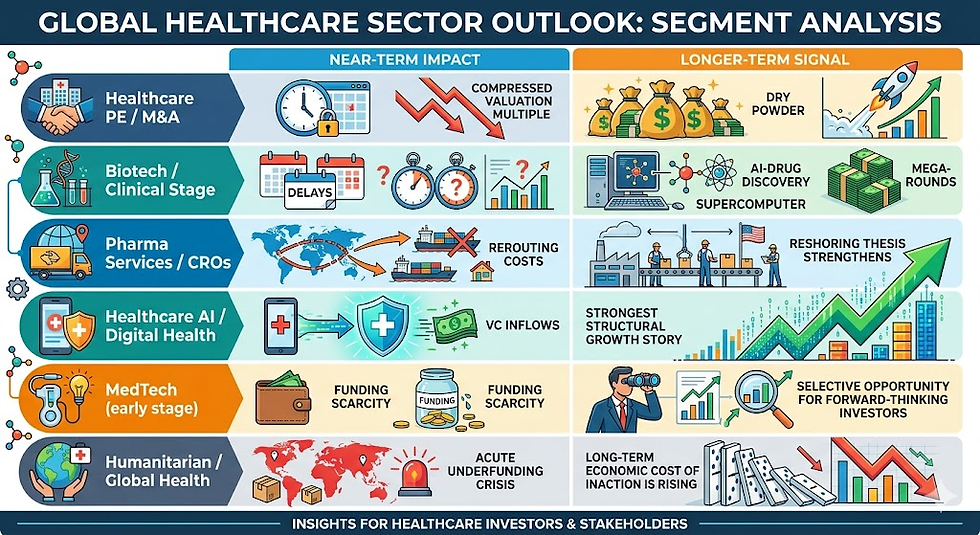

Market landscape

VC and M&A activity have declined in both total deal count and value over the past three years, while partnerships show fewer deals but higher total deal value. This shift represents a significant change in the investment landscape, as members at BROTHERS & Partners have identified the following investment trends:

- Investment trends :

Late-stage deals take the spotlight.

Rare diseases, next-gen modalities, and AI/ ML lead the charge

Risk reimagined with milestone-based licensing models

Chinese biotech out-licensing gains momentum

Why

Reduced risk appetite among investors and therefore focus on companies with clear commercialization pathways for immediate ROI

Rare Disease: Faster regulatory pathways and lower competition

Next-Gen: Curative potential offers differentiated clinical value

AI/ML: Scalable, Cost-efficient early-stage R&D processes

Limit financial exposure while preserving strategic flexibility across the pipeline

Pursue cost-effective pipeline diversification by sourcing promising preclinical or early clinical-stage assets from China

The facts

• Later-stage VC deals rose from 25% in 2023 to 31% in H1 2025

• $180B in drug revenue faces LOE by 2027-2028

• 52% of novel FDA approvals in 2024 were orphan drugs

• Next-gen modalities represent 55% of the projected 2024 pipeline value

• Biotech AI solutions drew $5.6B in 2024 VC funding—growing nearly 3× YoY

• Upfront payments were 8% in Q1 2025, down from 13% in 2019

• 32% of global out-licensing value originated from China in Q1 2025—up from ~21%

Four key VC deal trends:

Shift toward later-stage

• Later-stage VC deals rose from 25% in 2023 to 31% in H1 2025

• Capital markets remain constrained, with fewer IPOs and narrowing exit windows.

• As a result, VCs are concentrating capital in later-stage funding rounds. targeting companies with strong clinical data and clear commercialization pathways.

• This shift, driven by a reduced risk appetite, is leading to larger investments in fewer, more mature firms.

Examples: Zenas (2024): $200M • Alumis (2024): $259M

2. Next-gen modalities (e.g., RNA, ADCs)

• Next-gen modalities represent ~$170B (~55%) of projected 2024 pipeline value

• Investors are betting on next-gen modalities with curative potential (e.g., RNA-based therapies, cell and gene therapies, antibody-drug conjugates) that provide differentiated clinical value.

• These platforms offer strong M&A and IPO potential, orphan drug designations, and long-term exclusivity—particularly attractive in high-burden

disease areas with limited existing treatments.

Examples: ReNAgade (2023): $300M • Aera (2023): $193M

3. AI & ML-driven Drug discovery

• Biotech AI solutions drew $5.6B in 2024 VC funding—growing nearly 3×YoY

• Venture capital is accelerating into AI-native biotech platforms due to their ability to streamline early-stage R&D, reduce time to hit identification, and

Optimize compound screening.

• These companies enable multi-asset pipelines, platform licensing models, and data network effects, which improve scalability and long-term returns.

Examples: Xaira Therapeutics (2024): $1B • Isomorphic Labs (2025): $600M

4. Advanced rare disease therapeutics

• 52% of novel FDA approvals in 2024 were orphan drugs.

• VCs continue to fund high-impact rare disease programs targeting ultra-orphan and monogenic disorders due to faster regulatory pathways and lower competition.

• These therapies often secure premium pricing, strong payer support, and patient advocacy, creating favorable risk-reward dynamics even in niche

indications.

Examples: Glycomine (2025): $115M • Abcuro (2025): $200M

Suggestions for 2026 and beyond

To align with the evolving market landscape and investment trends, BROTHERS & Partners recommend:

Be proactive in market predictions to adapt to a changing landscape

• Leverage early signals and advanced analytics to anticipate investment shifts and keep strategies aligned with today’s dynamic, rapidly evolving market.

Focus on differentiated, fast-to-market assets

• Prioritize assets with clear clinical advantages and accelerated paths to market—avoid early-stage, high-risk programs with uncertain outcomes.

Structure capital-efficient licensing deals

• Use milestone-heavy agreements with minimal upfronts to preserve cash while capturing upside through royalties and backend economics.

Show up where deals happen • Focus on high-impact platforms like in JPM week, EBD Group, and LSX investor events - companies presenting there saw more than double the median deal value for both VC and M&A.

Comments